Curtain closing on Prime Money Market Funds?

In our previous blog post, “Are Money Market Funds the Safest Port in a Rough Financial Ocean” we discussed different types of money market funds and their benefits and shortcomings. In this post, we are going to do a deep dive into prime money market funds, since there has been an increase in news about them recently.

What is a Prime Fund

A prime fund has the same mutual fund operating structure as all other money market funds, but the assets they are permitted to invest in are slightly different.

Like many other funds, Prime funds largely hold US Treasuries and US Government debt, but they also have the unique ability to invest in corporate credit instruments. These include Bank CD’s, commercial paper, corporate bonds, and USD-denominated foreign debt issued by governments and corporations.

The ability to invest in these additional assets allows them to offer investors higher yields.

Rules of a Prime Fund

Money market funds are under the jurisdiction of the SEC and are regulated by the Investment Company Act of 1940. Furthermore, SEC Rule 2a-7 outlines the specifics of what classifies a money market fund.

Some of the basic characteristics are:

- Assets cannot have a remaining maturity longer than 13 months

- No more than 5% of total assets can be in illiquid securities

- A minimum of 10% of total assets must be daily liquid

- A minimum of 30% of total assets must be weekly liquid

- Portfolio holdings must be posted monthly on the fund’s website

October 2016 Reform

In October of 2016, the SEC enacted reform to the money market industry. The rule changes were an effort to keep money market funds resilient during a period of market turbulence and help reduce the possibility of large scale redemptions. Regulators sought to prevent a repeat of 2008, when the Reserve Primary Fund “broke the buck” and investors in funds lost money.

The SEC had prime funds right in their crosshairs as they implemented these changes, which ended up fundamentally altering the way prime funds operate to this day.

The changes made by the SEC were:

- NAV (net asset value) must accurately represent the current market value of assets. Prime funds can no longer tout a consistent price value of $1. i.e. NAV moves above and below $1.

- Prime funds may institute fees on redemptions during times of stress:

- If assets that can be liquidated in a week falls below 30% they can place a 2% redemption fee

- If assets that can be liquidated in a week falls below 10% they MUST place 1% redemption fee

- Once the 30% threshold is breached they have the OPTION to halt redemptions for 10 days

So much for liquidity anytime you want it!

Pros of Prime Funds

Generally speaking, there are two main benefits of a prime fund.

- Better yield than US government securities, because of the inclusion of corporate credit

- Fee free same day liquidity at the fixed NAV (or near the fixed NAV in some cases due to fees)

Cons of Prime Funds

Interestingly, the pros of a prime fund also are the cornerstones of their negatives.

- Floating NAV puts you at risk of redeeming shares for cash below your purchase price. This means you could lose some of your invested capital.

- In turbulent times, you may have to pay a redemption fee to get your capital back.

- The fund is operated by a fund manager, and people are fallible. The manager could mismanage the fund, go out of business, or simply close it down.

There are no guarantees the fund you are invested in will stay open and certainly no guarantees the fund manager will stay liquid.

A Better Way With SMAs?

Separately Managed Accounts are an investment account owned by a corporation or individual that is managed and monitored by an independent third party money manager. We believe SMAs offer distinct benefits over funds and that is why InterPrime chooses to use them.

Let’s take a look at what makes SMAs different from money market funds and mutual funds.

Transparency

When you use a SMA, you have full transparency into the account. You can see each holding and transaction in real time. When you own a fund, you see all of this important information after the fact, and only once a month!

Control

A SMA allows you to control and own assets directly. When you participate in a fund, you only own shares of that fund, nothing more. In an SMA, you own the assets you want and keep them separate from other individuals or corporations. Avoiding commingling of assets reduces risk.

Customization

SMAs are not a cookie cutter solution. They can be customized and adjusted for each individual or corporation. You are not buying an off the shelf product. In an SMA, you have the ability to require or prohibit certain investments. In a fund, you get what you get - no customizations.

Cost

Being bespoke, most investors think they will incur high costs to have an SMA. SMA costs are competitive with, and in some cases less expensive than off the shelf funds.

SMA vs. Prime Funds

To illustrate the advantages of an SMA over a prime fund, we are going to outline a brief example.

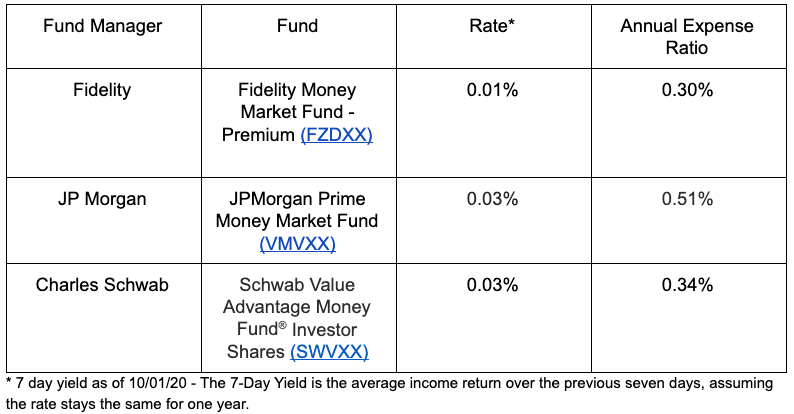

Charles Schwab, Fidelity and JP Morgan are household names, and are also some of the biggest prime fund managers.

Below are their prime funds, the returns they are currently paying* and the expense ratios they charge.

We believe the difference between the expense ratio and the payment rate is absurd. The fees on the funds produce a drag on returns by absorbing most of the potential returns.

At InterPrime, our fee is based off of the investment policy you choose. The top tier custom investment policy is 0.25% annually. The other standard policy options are lower fee.

Why Are Prime Funds Closing?

In recent years, many prime funds have been steadily closing down. In March, when the coronavirus pandemic first hit, there was an additional uptick in prime fund closures.

Fidelity, one of the largest prime fund managers, announced closures back in July. Northern Trust also decided to shutter some in May. Even Vanguard changed the model of their prime funds in August.

But why?

Most of the anecdotal evidence shows that during the March 2020 stress, investor redemptions had prime fund managers on their heels. They worried about possibly having to enact those redemption fees that we mentioned earlier. In some cases, they even had to flood the funds with their own proprietary capital to stave off redemption fees.

In addition, firms like this depend upon their reputations. They do not want to incur the negative PR of one of their funds going awry. Such incidents undermine investor confidence and make it harder to gather assets in the future.

The structure of a prime fund allows it to take on more credit risk via non-government assets. With yields currently so low, firms seem to be calculating that offering higher yield is not worth the extra risk right now.

The last word

Financial markets move in cycles and it appears the cycle may be closing on prime funds. Their creation was well-intentioned but the current interest rate environment and adjustments in regulations have significantly diminished their viability.

We strongly believe there are better ways to achieve the same investment goals.

Our preference is to use SMAs because of their customizability and seamless ability to adjust when needed. Every cash manager and corporation is different, so why buy off the shelf products?

If you currently have money in a prime money market fund, it might be worth exploring other alternatives. We are always happy to discuss your current cash management plan and offer our input with no obligation to you. Simply shoot us a message.