Snowflakes in September - An analysis of Snowflake's corporate cash

Snowflake IPO'd as the hottest new company to come public in 2020. Salesforce and Berkshire Hathaway invested in the IPO, knighting Snowflake as "best of breed". Let’s dig into Snowflake’s S-1 to see how they manage their corporate cash!

If you are a founder, CFO, or manage your company’s corporate cash, take note. The lessons here are applicable to companies of all sizes.

Before IPO Snowflake had $886.8mm in “cash” on their balance sheet. Did they keep all that in a Bank of America checking account? Of course not. They know once you have more than $250k in a single bank account, you lose FDIC insurance protection. Instead, they focussed on maximizing the safety & security of their cash by investing it and earning a reasonable rate of return on their capital.

This line comes straight from their S-1:

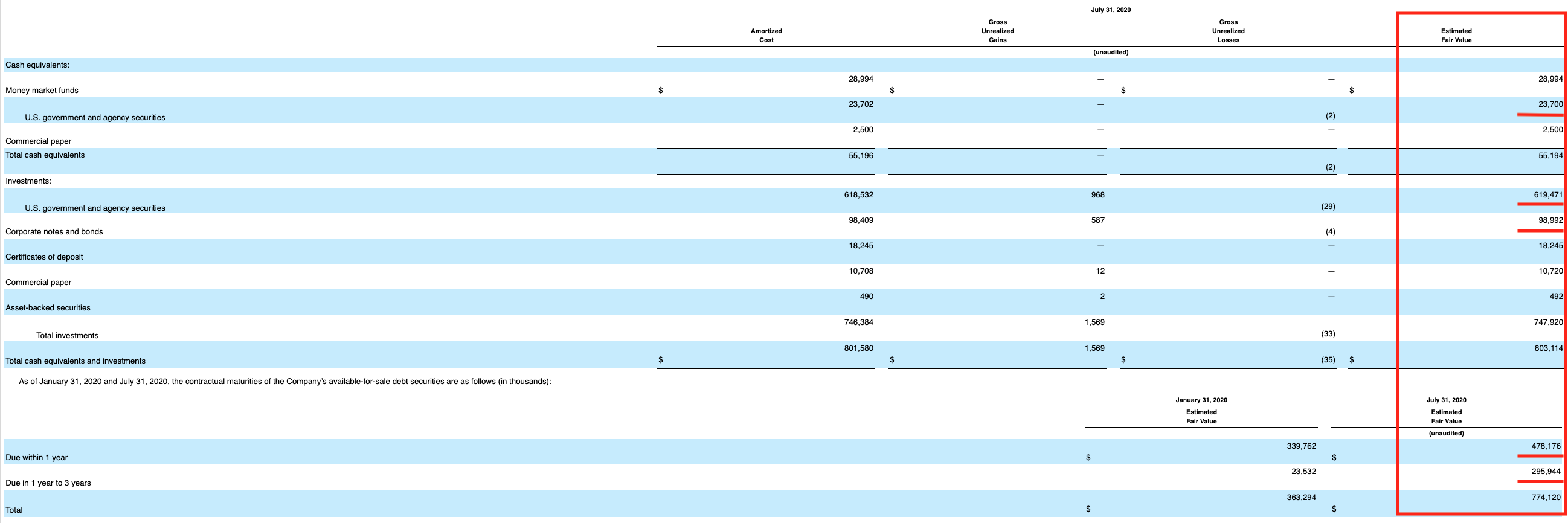

“Our investments consist of U.S. government and agency securities, corporate notes and bonds, commercial paper, certificates of deposit, and asset-backed securities.”

Some back of the envelope calculations show that they have approximately:

- Cash ~$83M

- Cash Equivalents ~$55M

- Short term investments (less than 1 year but more than 3 months) ~$423M

- Long term investments (less than 3 years but more than 1 year) ~$295M

The lion's share of these “investments” are in U.S Government Bonds for safety, security and liquidity. They even go a step further by sprinkling in high quality, investment grade corporate bonds and some bank certificates of deposit. These assets help to increase the “interest income” on the cash they hold.

They have earned ~$4.1M in interest income alone in the first 2 quarters of 2020 (source: S-1). Not too shabby!

From a structuring standpoint, Snowflake appears to only keep enough liquid cash on hand to keep things rolling near term. Everything beyond that is invested out into the future to earn them more on their money.

Now, you may say, “Hang on. Snowflake is a multi billion dollar business. Of course they need to invest that capital, but my business is only a fraction of that size” To that we say it is never too early to start managing your cash like the best. Even if your numbers are much smaller, you’ll establish good practices that will serve your business well as it grows.

Our goal at InterPrime is to help all companies operate like Snowflake or a Fortune 500 business. You may not need to use every asset class they use. But it’s best to consider what they are doing and leverage some of their techniques to make the most of your capital.

Do not consider this a prescription but a simple illustration on how you can follow their lead.

- Be wary of having more than $250k in any single bank account. Amounts beyond that put your cash at risk.

- Amounts beyond $250k can be directed toward US Government securities. Those offer next day liquidity and unparalleled safety.

- If you have cash visibility out to 6 months or longer, you can explore Bank certificates of deposit and high quality investment grade corporate bonds to increase the income on your excess cash. Think of them as a “no touch” until 6-12 months.

Again, this is not a prescription but a way to think about how to keep your cash safe and earn a reasonable rate of return. Reach out if you would like to discuss how InterPrime can help you manage your corporate cash.

Appendix: relevant sections from the Snowflake S1