The Bond Market - The Market that moves all markets

For every action there is an equal and opposite reaction - Newton’s Third Law

Newton’s Third Law is a physics fact but in investing you see similar reactions. News stories, earnings reports, environmental crises and tweets seem to affect the markets on a daily basis. If you are able to understand how assets are correlated, you will be a higher level investor.

This note is going to speak about the relationship between bonds and all other markets. The goal is to give you a better understanding of how bonds decide much of what happens in the finance world.

What is the Bond Market?

Everyone knows what the stock market is but not all investors know about the bond market. So what is it?

The bond market is the global marketplace to buy and sell debt securities. You may also hear it called the fixed income market, credit market or debt market. The names are different but they describe the same thing.

The purpose of the bond market is to provide a way for governments and companies to raise money. They do this by issuing bonds that investors buy. Investors like bonds because they are a contract between the issuer and themselves. In return for giving the government or company cash, investors receive fixed and consistent interest payments based on the contract. When the contract completes the investors get all of their principal back to reinvest!

Both the issuer and the bondholder win. The government or company gets the funding they need/want and the investor has an investment that pays them.

If you want to learn about the history of the bond market view our previous post here. We walk you through the start in Mesopotamia in 2400 B.C. to the Venice evolution in 1100 A.D.

Why is the bond market important?

All things evolve and so did the bond market. What started out as a simple way for governments and companies to gain cash, has grown into something much larger.

Now the bond market affects the whole finance world. From how asset prices are set, to how money flows around the world. Let’s look at how that happens.

Bond Market and Security Prices

Investing is a function of two things:

- Understanding the relationship between risk and reward.

- Knowing when an asset's price is appropriate versus the risk you are taking.

Bonds are an important part in how investors view both.

How Bonds Change Investor View on Assets

Because bonds have a predetermined cash payment schedule and maturity date. Investors can use a valuation formula to determine if the current price of the bond they are looking at is worth owning for their needs. Straightforward analysis.

When an investor is looking at other assets - stocks, real estate, private companies etc. There are many variables that go into calculating current and future expected value. Current and future cash flows for example. Because of this uncertainty, calculating valuations becomes more difficult.

If the analysis of the non bond asset presents the likelihood of a favorable investment outcome. The investor may place their chips on that asset over a bond.

Over time investors monitor and re-evaluate their investments/assets. During re-evaluation similar analysis that got them to purchase the asset is redone. If variables have changed, like bond rates, what previously was an interesting investment may now not look as good. In that situation, the investor may decide to sell the non bond asset.

This process of analyzing assets consistently and then changing between assets is called rotation. Rotation is what keeps some assets in favor and rising in price. While others falter and go lower in price.

This rotation process is happening constantly. Being aware how different assets react to bond rate changes is crucial. It can help you find assets that are poised to appreciate. Or help you exit investments that can hurt you when rates change.

Bond Markets Anchor the Money Flow

“Earnings do not move the overall markets; It’s the Federal Reserve. And whatever I do, focus on the central banks and focus on the movement of liquidity…..it’s liquidity that moves markets.” - Stanley Druckenmiller

The reason you focus on the central banks is because they set short term rates which all other bond rates are based on.

In times when they set rates at low levels - like currently - the cost of capital is cheap and the desire is high. Companies take advantage of this and get cheap funding to retire more expensive debt obligations (like you do with a mortgage refi) or use the funding for future growth.

In times when rates are set at higher levels. The cost of capital rises so corporations start pulling back on borrowing. This in turn slows down the flow of money to expansion and growth projects.

Because central banks can change the rates the bond market pays. They, and the bond market, set where money flows in the world. Both for corporations and individuals.

Real World Examples of Bond Market In Action

The following sections give real world examples of how the bond market connects to other markets.

Tech Stocks Hit When US 10-year Yield Rises

Stocks saw a strong recovery after the COVID pandemic thanks to government stimulus. The rally in tech stocks has been amazing and only recently hit a road bump. But why? The reason is because longer term bond yields rose.

The US 10-year bond yield has risen since August 2020 with a rapid advance through March 2021. One of the reasons this happened is because investors are concerned inflation may rise due to government stimulus and the economic recovery.

Tech stocks thrive when interest rates are low. This allows them to get growth funding at a cheap price which increases the speed of company growth. With forward looking growth all but guaranteed. Growth investors pile into the tech names. That is until they get scared interest rates will rise and the cheap funding goes away.

When the cheap funding goes away the calculations regarding future valuations are affected. What previously looked like hockey stick growth may now only be a small ramp or flat line. This effectively tells investors that current prices of these companies are too high. Investors then may take profits or sell and back away completely.

The below chart shows the US 10-year yield rising rapidly in Feb-Mar 2021 and the impact it had on the Nasdaq. i.e. it sent the Nasdaq down -10% to correction territory.

We will need more time to see if the inflation fear is real. Investors' worries have calmed somewhat recently. But any further indications inflation is coming, wIll likely send tech stocks on another leg lower as bond yields rise.

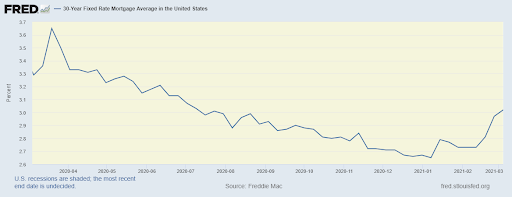

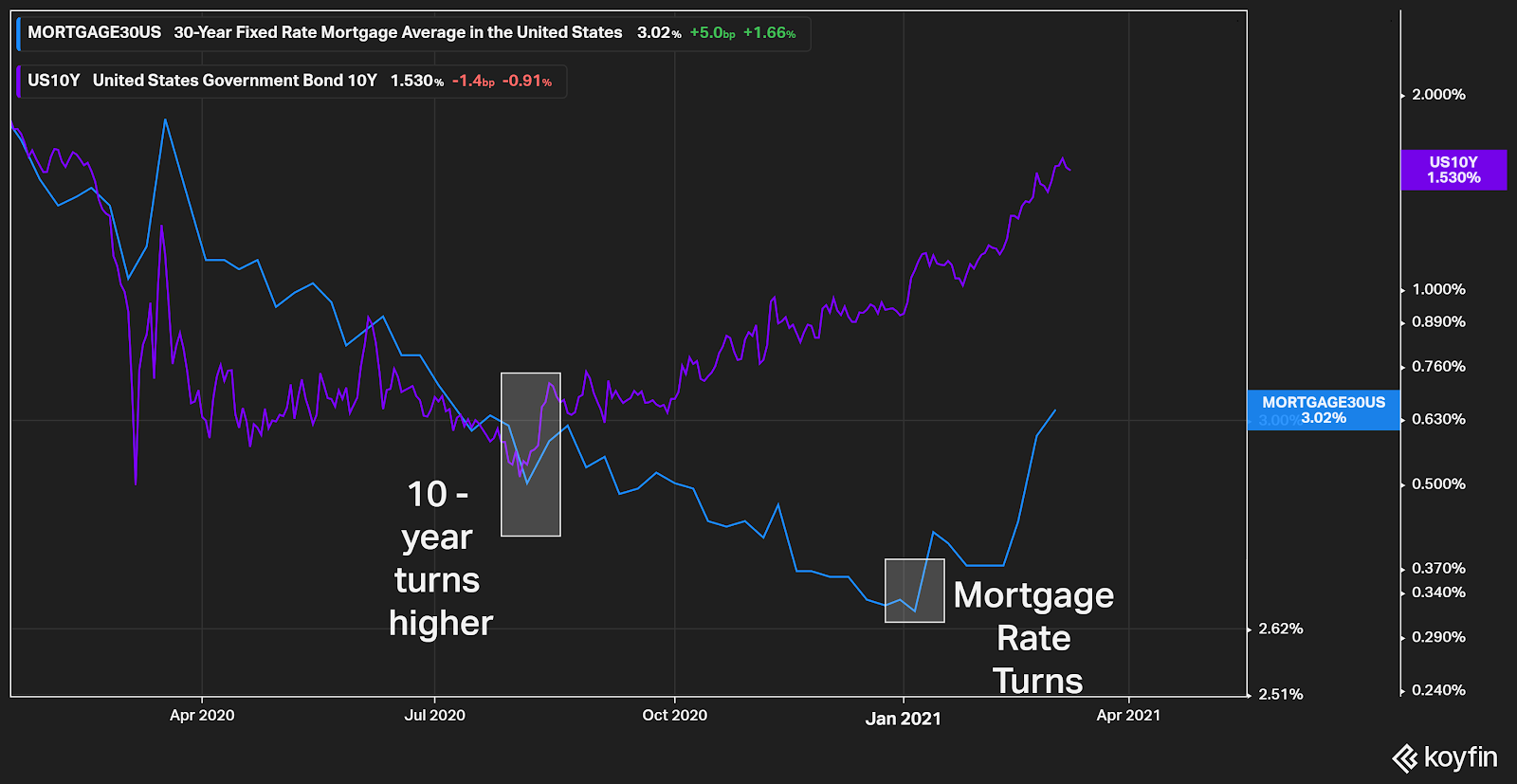

Bond Yields Direct Mortgage & Refi Rates

While bond yields going higher hurts tech stocks. They also drive the health of the mortgage and housing market.

Mortgage and refi rates are set off of multiple variables including the US government 10-year and 30-year bond yield. The way mortgage lenders do this is as follows: they take the government rate - say 1.50%. They then add an extra percentage on top to build in costs, fees and profit. Say 3% for a 30-year mortgage. In this example they keep 1.50% difference in the rates for themselves.

The below charts show how the 10-year government bond yield started to rise last year. Then the 30-year mortgage rate started to track it higher in Jan 2021. With an acceleration higher till now (Mar 2021).

If the current trend continues. One would assume mortgage rates will continue to rise with the 10-year Treasury. There will be a tipping point when mortgage rate increases affect new home mortgage applications and refi applications. We are starting to see hints of this now.

It is worth mentioning that the use of 10-year Treasury as a mortgage rate benchmark is because most mortgages will see a refi in year 10.

Bonds and Bank Loans

What is happening in the bond market also changes how much a bank loan will cost you. We touched on this in the mortgage and refi section. But it is universal for other bank loans. The process of getting a bank loan revolves around a few key points. Amount requested, term of repayment and borrower risk.

Amount requested is straightforward as loans are specific to a need. Like a new car for example. The term of repayment is also usually known at the start. i.e. 5-year or 7-year in the car example. The credit risk of the borrower risk is where things get murky.

A bank lending team will assess you or your company's potential to repay the bank based on many factors. These include credit score, history of paying existing creditors, amount of assets, etc. All these factors help the bank determine IF you will be able to repay the loan.

The bank starts by matching your desired repayment term with bonds maturing in the same time frame. i.e. A 5 year loan term will match what a 5 year maturing bond is paying. Once they have an idea of what those bonds are paying the interest floor will be set. They then add on administrative fees and the profit they try to make off of the certain loan type you are requesting. They then factor in the borrower risk profile they created.

If you are a star borrower who always pays creditors on time, has lots of assets, and has clear cash flow coming in. The bank will likely stop at the current analysis and present you an offer. Being a star borrower gives you power to negotiate and even see the bank reduce part of their profits to gain you as a customer.

If you are not a star borrower things tend to get worse because they see you as a potential risk to not paying them back. They will increase the interest rate on the loan to compensate them for the perceived risk you will not pay. i.e. their profit take increases to make them feel comfortable with you as a customer.

The main take away from this section is the initial floor of what your bank loan will cost comes from the bond market. How good or bad your loan terms will be is decided by you or your company’s credit/risk profile.

Wrap Up

The stock market always gets the TV coverage and excitement. But the bond market is where things matter.

From the central banks setting rates to change the money flow. To the bond market deciding how much your bank will charge you for a loan. The bond market is pulling the levers to decide asset price direction, and how investors use their capital.

After reading this we hope that you start to pay more attention to the bond market. Knowing when the bond market changes gives you insight to how the economy and your money will perform.

If you would like more educational and entertaining posts like this one - please subscribe to our our newsletter.