Using Bond Ladders to put your idle cash to work

“It takes money to make money”

Some people believe it to the letter. While others completely disagree with it. The truth is somewhere in the middle.

The tools and strategies to grow the money you have move along a risk spectrum. On one side are speculative high risk where you hunt for home runs. On the other side are conservative slow grinders with reduced risk and potential for consistent profits. Neither is better than the other. You only need to understand the risk and potential outcome going into it.

This post will explain one of the more conservative strategies that can create cash flow and income. It is called a bond ladder and it can be used by companies and individuals.

If used correctly, the cash flow and income created from a bond ladder can:

- Pay Expenses

- Fund Business Objectives

- Pad Emergency Funds

- Extend the Life of Your Business

The beauty of a bond ladder is anyone can use them once you understand how to do it, and the income coming from them is consistent and can be counted on.

What Is a Bond Ladder

A bond ladder is a portfolio of bank CDs or bonds that mature at different times in the future. The strategy focuses on providing income while also reducing risk from changes in interest rates.

Buying bank CDs or bonds with different maturity dates forces you to stick to a plan. This keeps you disciplined and prevents you from trying to time the market. It also allows you to know when and how much you will get paid via coupon payments as well as principal payments.

As long as you reinvest the cash from each maturing bond. You can create a near perpetual money machine that pays you.

Benefits of a Bond Ladder

Create & Manage Cash Flow

Since bonds can pay you monthly, semiannual or at maturity. You can design and structure your bond ladder in any way you want or need.

Want monthly income? Check!

Want your bond ladder to cover a certain expense? Check!

Want your bond ladder to give you a lump sum payment in the future? Check!

Manage Interest Rate Risk

Interest rates change often, and sometimes dramatically. When you build a bond ladder with different maturity dates, you avoid locking in any single rate for a long time. The staggered maturity dates smooth out the fluctuations in changing interest rates.

Each time a bond matures you go to the market and purchase a new bond with a maturity date in the future. If rates have risen, you lock in a new higher rate for that portion of the ladder. If rates have fallen, you will unfortunately buy a lower rate. However, bonds already in the ladder will have previously locked in higher rates.

Building a Bond Ladder

Bond ladders are simple and straightforward to create. The 3 main pieces to building one are:

- Rungs

- Spacing

- Investments

Rungs of the Ladder

Deciding how much you plan to invest in a bond ladder will determine how many rungs it will have. This also decides how far in the future the ladder can be and how often you get paid.

Example:

$1,000,000 for bond ladder strategy could give you 10 $100,000 rungs

Each $100,000 rung would purchase an individual bank CD or bond

Tip: Most CDs and bonds pay you 2 times a year (semiannual). If you have at least 6 rungs of the ladder you can build it so you can get paid every month of the year.

Rung Spacing

Rung spacing is the time between the maturities of each bond. It is ideal to try to keep the time between maturities near equal.

Longer maturing bonds will generally pay you more. But they also increase your interest rate risk. You can reduce interest rate risk by shortening the bond maturities of the bond ladder.

Investments

A bond ladder can be built with various fixed income instruments. Each flavor has a different benefit.

Here are the most common:

- Bank CDs

- US Treasuries - credit guarantee from the US government

- Municipal - potential tax advantages

- Investment Grade Corporate - increased yield and liquidity

- High Yield - increased yield

Tip: It is best to build a ladder out of higher rated bonds. A high yield bond can offer you increased yield. But they come with increased risk of default. Defaults can affect the goal of consistent income and if you get your full investment back.

How a Bond Ladder Works

Remember, with bond ladders you invest in multiple bank CDs or bonds with different maturities. As each bond matures, you reinvest in a new bond with the longest maturity you picked for the ladder.

If interest rates rise, you buy a new bond with a higher rate. If interest rates fall, or stay the same, old bonds are locked in at a higher rate.

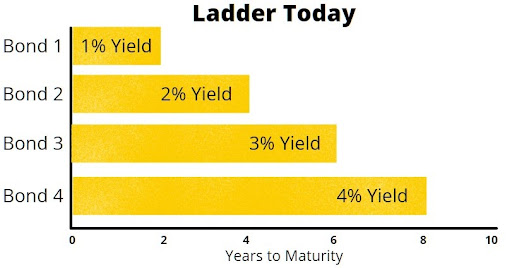

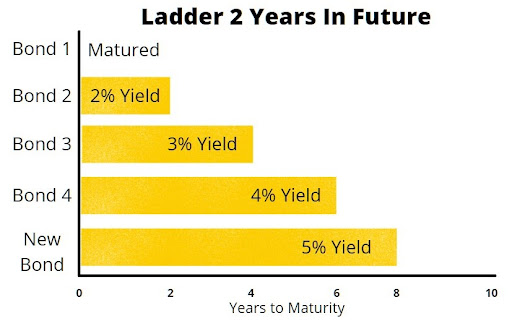

The below example is hypothetical for illustration. We picked 8 years for ladder length. With 2 year rungs.

Two years in the future, Bond 1 matures. You reinvest that money in a new bond at the maximum maturity. In this example, rates rose - hurray!

You would continue this process for as long as you wanted the ladder in place.

Wrap Up

There are a million strategies and tools to make money investing. The bond ladder is one of the more conservative ones. You build it how you want, and have a reasonable expectation of what you will get.

The various fixed income assets and maturity dates help you customize it. All while letting you manage cash flow and reduce your interest rate risk.

If you value cash flow and income you may want to consider a bond ladder. They can help you both personally and for your company.

Reach out to us if you have any questions. We are happy to help you learn about bond ladders.